Not all people are users, but all users are people

The Pensions Advisory Service (TPAS) and Teamspirit believe that designing for people should be at the forefront of all financial services development. With technology providing unparalleled innovation, we need to foster collective responsibility across the industry, creating more human and engaging connections with those we exist to serve.

As TPAS would say, it’s vital we “Keep the people in pensions”.

In a world where so many remain under-served and unsure, the TPAS and Teamspirit event shone a spotlight on the very human needs that should drive financial services. Happily, we are not alone in our thinking, and our panellists and “podsters” showcased just what can be achieved when the customer is placed at the heart of products, services, experiences and communications. Their input was an invaluable part of the day and of this report, and we are very grateful for their support.

Design for people

In writing this report, we have made some assumptions about you, the reader. We have assumed that you understand English, you have a grounding in financial services and have experience either as a designer or as a user of financial services. We assume that you are motivated to learn more and gather insights from others.

These all seem like reasonable assumptions. Perhaps in this context they are, but often the assumptions that we make in financial services, are based on our view of the world and what we believe customers need. It soon becomes apparent that our kind of thinking, and all the “givens”, are far from people-centric when it comes to designing financial services products, tools and services. Rather they are centred on the needs of the industry.

It is rooted in old management paradigms of operational excellence and management by objectives, many from a previous industrial age. It holds the premise that we know what the customer needs and the customer should be grateful for the services that we provide. But the world has changed. People no longer put up with impersonal mass production in the way they used to. Some of our least favourite customer experiences are with faceless institutions that end the conversation with “Is there anything else that I can help you with?” - even though the preceding conversation had been fruitless and unhelpful.

“New agile ways of working and fast prototyping, testing and learning give no excuse for bad design.”

People have many new ways of making themselves heard when things are poorly designed or just designed for someone else. Customers turn to social media. There is less respect for organisations and authority figures, which just tell us how it is rather than investing in finding out what people want. New agile ways of working and fast prototyping, testing and learning give no excuse for bad design.

Most of all for new businesses that have been built with a higher bar for customer service and propositions centred on making life easier for users. But not all customers are in the same position. Not all are empowered or confident enough to rail against a lack of empathy. Not all have a voice. In our work at TPAS, we hear this every day and we are reaching a motivated minority; many more will quietly suffer later life in particular, because we never put those people at the centre of financial services that were developed decades ago.

An example from Design that Matters

Jaundice affects two thirds of new-born babies. If it is not treated it can lead to disability or death. However, there is a very cheap, low-cost cure – phototherapy.

Timothy Prestero, founder and CEO of Design that Matters, partnered with a medical research institution to design the NeoNurture incubator, that can work in less developed countries. Despite winning many awards, it did not work in less developed countries. Why? In the UK, a single jaundiced baby is placed in a phototherapy device. In Kathmandu, three babies would be put under one device. Then the mother would see her baby naked and put a blanket over it – reducing or even negating the phototherapy benefits.

So Design that Matters needed to pay more attention to the families, the doctors, the nurses and the repair technicians who were going to use the equipment.

The device was redesigned to be cheaper, more robust, with lights above and below and fit only a single baby. In other words, the right way to use it became the easiest way to use it.

So what can this teach us about designing financial service products? We need to make them simple, intuitive and relate to people.

In 1993, the Pension Law Review Committee, recognised the importance of pensions increasing in payment in order to keep pace with inflation. In April 1997, it became an obligation for defined benefit schemes to increase pensions in payment. This better protected the member in retirement, especially as the period in retirement was becoming much longer. Defined benefit pension schemes were starting to pay out a more expensive pension for longer. We started to see defined benefit pension schemes close, as the cost to the employer of these schemes spiralled – not helped by economic conditions, other changes to benefits, investment and technical provisions. During this time the Government also needed to change the structure and starting ages of the State Pension.

Whether the cause was the member protections or members living longer, the result was a demise of the defined benefit scheme. We are now living in an environment where the responsibility for having sufficient income has shifted well and truly from the state and the employer to the individual. If it is the individual’s responsibility to plan to have sufficient income for the retirement they want, they have to plan.

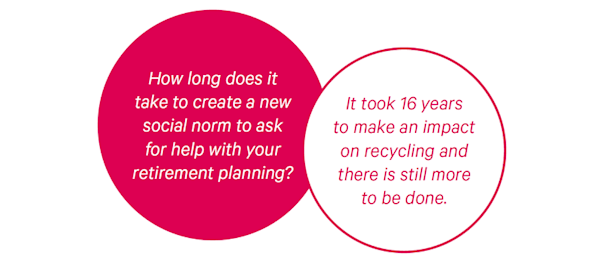

Easy! Not quite: it becomes easy only when it becomes a habit, a new social norm to plan for your own retirement.

How long does it take to create a new social norm? In 1993, recycling was a fairly marginal activity in the UK, where less than half of households regularly recycled paper and only a quarter regularly recycled cans(1). By 2009 it had become a more normalised activity, where 90% of households normally put out paper for recycling and 80% did so for cans(2). It took 16 years to make an impact on recycling and there is still more to be done.

Financial services has a weaker starting point than recycling. People saving into pensions and other financial services products have been let down by scandals, high charges and complexity, so trust was lost. Recycling might be in the same danger, given reports of green bags just being tipped into landfills!

By 2035, over 65% of people will be retiring, with defined contribution pot pension provision making up all or a proportion of their retirement income. The timescale for helping people with their pensions is even more challenging, because it is about capturing people 15-20 years before retirement and making them see retirement planning as the social norm that people engage with throughout their working life, particularly in the mid-40s to mid-50s age range. We need to make retirement planning:

● simple to do and hard to do wrong;

● radically more efficient and effective, so that people see the benefits;

● consistent, so that people are not bamboozled by changing fads; and

● accessible to all.

- Defra. Survey of Public Attitudes to the Environment. London; 1996

- Thornton A. Public attitudes and behaviours towards the environment – tracker survey: A report to the Department for Environment, Food and Rural Affairs; 2009

Customer insights from TPAS customers

< Most of us would like to be able to choose to stop work one day and choose how we live when we do. A decent pension is a good way to achieve that. Our vision is a future where people are empowered to make the most of their pensions. Our work is not only about knowing the answers to the questions that our customers ask, but also about delivering a service that is designed with the needs of our customers in mind.

The work starts before people call us up. Most people know that it is important for them to think about their retirement income. A need does not automatically translate to a demand. We find ways of being present at places where people may be thinking about their pension. This takes us to outreach events, raising awareness through social medial and making sure that our website is high in organic search. We also know that most people ask their friends for help, so we ensure that we have a high advocacy score and that people who have used our service proactively recommend us.

● The presenting question is often not the real issue that the person should be considering; the guider needs the pension specialist knowledge to diagnose the real issue.

● People want the help to be personal and tailored, so it is important to offer “one-to-one” help through channels such as telephone and web chat, as retirement circumstances have important differences.

● Guidance needs to be offered on an independent and impartial basis, so that people can trust the information that they are given and feel able to share all the relevant facts.

● Guidance needs to be actionable; too many next steps will result in inaction.

● People need the questions that they need to ask of themselves or others, so that they are confident to take the next steps.

We collect customer insight data, in order that we can track trends and identify any areas where there is an increase in questions and issues. Each year, we share our insight in our Annual Review, so that we can help all parties involved in pensions to provide a better service.

Good pensions can change people’s lives. Independent and impartial guidance helps people have good pensions.

Great examples of what customers love

Overnight currency collection from John Lewis Finance at Waitrose

“Can’t tell you how handy I find being able to order my currency for travelling online and collect it the next day or whenever it suits me from my nearest little Waitrose. Ditto new socks and pants for the kids. An invaluable tie-up based on realising that I’m time-pressed and need to have confidence that promises will be kept.”

FairFX pre-paid currency card

“There are lots of options out there, many with caveats like having to shift your current account. FairFX lets me take advantage of pre-buying currency at a great rate and having the security whilst away of not needing to carry cash or be ripped off by withdrawal fees.”

bpay wristbands designed for festivalgoers

“The bPay wristband is brilliant, especially if you’re an avid festivalgoer like me. When I’m in the fields it’s so much better to wear my band than carry around a load of cards. I can’t lose anything then! And it’s fast so I’m not holding up the queues paying for my burger and chips.”

NatWest Emergency Cash

“NatWest’s Emergency Cash has (almost) literally saved my life on more than one occasion. It’s a brilliant example of a brand innovating from a consumer’s point of view to create a genuinely useful service. One criticism? Not being able to use it after reporting your card missing seems counterintuitive.”

Apple Pay

“Just so convenient. I’ve never had any issues with it. Part of me panics as it’s not my bank card but as I always have my phone, for the way we live our lives now, it’s so much more convenient. I hardly ever carry cash around. It’s something I just don’t need to think about. Really does make life easier.”

A few examples from history:

Too slow to change – Blockbuster

Dave Cook opened the first Blockbuster in Dallas in October 1985. It was an immediate success: it had more tapes in more titles, displayed its titles on shelves and opened late – unlike its competitors. It used a computer system and scanner to track tapes and ease checkout. So where did things go wrong? Blockbuster stopped looking at the experience of its customers and the technology they were now turning to. While Blockbuster was keenly aware of the impact the internet, it acted too slowly. The format it was wedded to soon became extinct. Fundamentally, it stopped designing its offering around its customers and their experience.

Losing empathy with customers – M&S

The food business shows just what M&S is capable of. It is motoring at a time when many food retailers are struggling and the hard discounters are gaining share fast. The problems are in general merchandise. Shoppers, even in M&S’s over-50s customer base, are now much more choosy and much more demanding. They no longer have to give second best the benefit of the doubt, because they can check online to see what other retailers are offering.

Not designing for people is costly! Choice is only a click away.

What the podsters at our event think

At EValue we’re passionate about providing ways to help people make better financial decisions. Our insight asset model, calculation engine and advice engine help people see their financial futures and understand the trade-offs between investment risk and return. While providing accurate and robust numbers is the backbone of our business, it is not worth a jot unless we engage consumers.

- Tangible value – Consumer response to “get a free financial plan” can be 10X higher than to “speak to a toprated local adviser”.

- Goal-led – Starting an interaction with someone’s specific “goals” will often drive higher engagement than starting with their finances.

- Human experts – Most people need support from (and accountability to) a human, to stay committed to a complex or tedious process.

- Accessible – While few people will proactively request help from an adviser, many more will engage if they “cross paths” with one – for example, in a workplace.

- Affordable – People under-estimate the value of advice – requiring it to be ultra-affordable to achieve mass engagement.</p>

With Hatch, we have built technology that allows Financial Coaches – who can be trained in weeks with no prior financial experience – to produce robust, engaging financial plans for the majority of people (with non-complex needs). We provide Hatch in workplaces, driving high engagement, with costs reduced through the Pension Advice Voucher salary sacrifice scheme.

All phantom of course, but an aspirational design (and believe it or not an actual idea we have been exploring). It doesn’t mention pensions, but that is sort of the point we would support people in living their lives and reverse into pensions (to stimulate savings and drawdown.

This includes encouraging people to review and act with their pension which according to one of our customers’, she just would not have done otherwise. Into the future, we will be able to support payments through Moneyhub and allow people to sweep money from account to account without having to leave the app. It will truly be frictionless finance.

Design for people means not leaving behind professionals who choose to work for themselves, who choose to take care of their families and contribute to the UK economy as entrepreneurs. It’s designing solutions that embrace their values of flexibility, autonomy, mobile, efficiency; while also encouraging behaviour that helps them prepare for their future, even in times of short-term instability and stress, when they’re least likely to think about themselves.

We are just scratching the surface of how AI and roboadvice can improve how we manage our finances. The UK is on the brink of a savings and retirement crisis, which will impact the companies we work for and the society we live in. Wealth Wizards was founded in 2009, on the belief that everyone should have access to affordable financial advice, regardless of income. Since our founding we have used technology to help people better manage their savings and build confidence in their financial future. Wealth Wizards believe we can avert the savings and retirement crisis with the use of technology.

Thoughts from the day

Five golden themes

- Keep it Simple – However complex the subject matter, it can often be presented in a simple, straightforward way and with a helping hand to take you through the key points that matter to you.

- Make it Easy to Use – We are living in a time-pressured world and we are impatient. We want to swipe, tap and watch across devices – customers rarely want to be asked to read reams of information.

- Engage – It is clear that identifying a need and building a solution are not enough. You need to engage with your audience, to show them why this is a product and service that they cannot live without.

- Be Positive – People want to feel positive, and when a provider of a service shows that they are looking out for you, it creates loyalty.

- Be Visual – We buy with our eyes, so the design of the product is important. It should look styled to the audience and enticing, as the first impression really counts.

James Maxwell

While our partnership with TPAS may have helped focus our mind on pensions, what was clear from the popularity of the podsters, our insightful discussions and the enthusiasm of all attendees, is that the need to design for people across financial services is obvious to all.

From the products and services we create, how we engage then communicate, what form it takes, even to the language we use, we have work to do across the sector. While it can feel like a big task, what is heartening is the enthusiasm everyone has, as well as the willingness to learn from each other. At Teamspirit, we believe that it is creative collaboration that transforms. And when it comes to designing for people, this seems to be the way forward.

Michelle Cracknell

At TPAS, our belief and experience are that most people realise that pensions are important. But they can be complex and difficult to understand, which is why our hypothesis for the day was, “People are interested in pensions; we need to do more to ensure that all products and services are designed for people.” In addition to the five golden themes that surfaced, attendees also expressed enduring issues and concerns about security, trust and access to information. But the overriding feedback was an enthusiasm that financial products and services are, and can, be designed with people at their heart. Of course, one event is never going to find the solution to the conundrum of how to make pensions interesting, but we hope that the audience left with renewed motivation to “Design for people”.